Overview

Loan Origination Solution (LOS) is part of an industry-leading digital banking solution suite that is used by banks in around 100 countries to serve over 1 billion customers. Origination is a lengthy process followed by the banks to investigate the financial health of the borrower. This helps the bank negotiate terms of the loan and agree upon the loan amount to be offered.

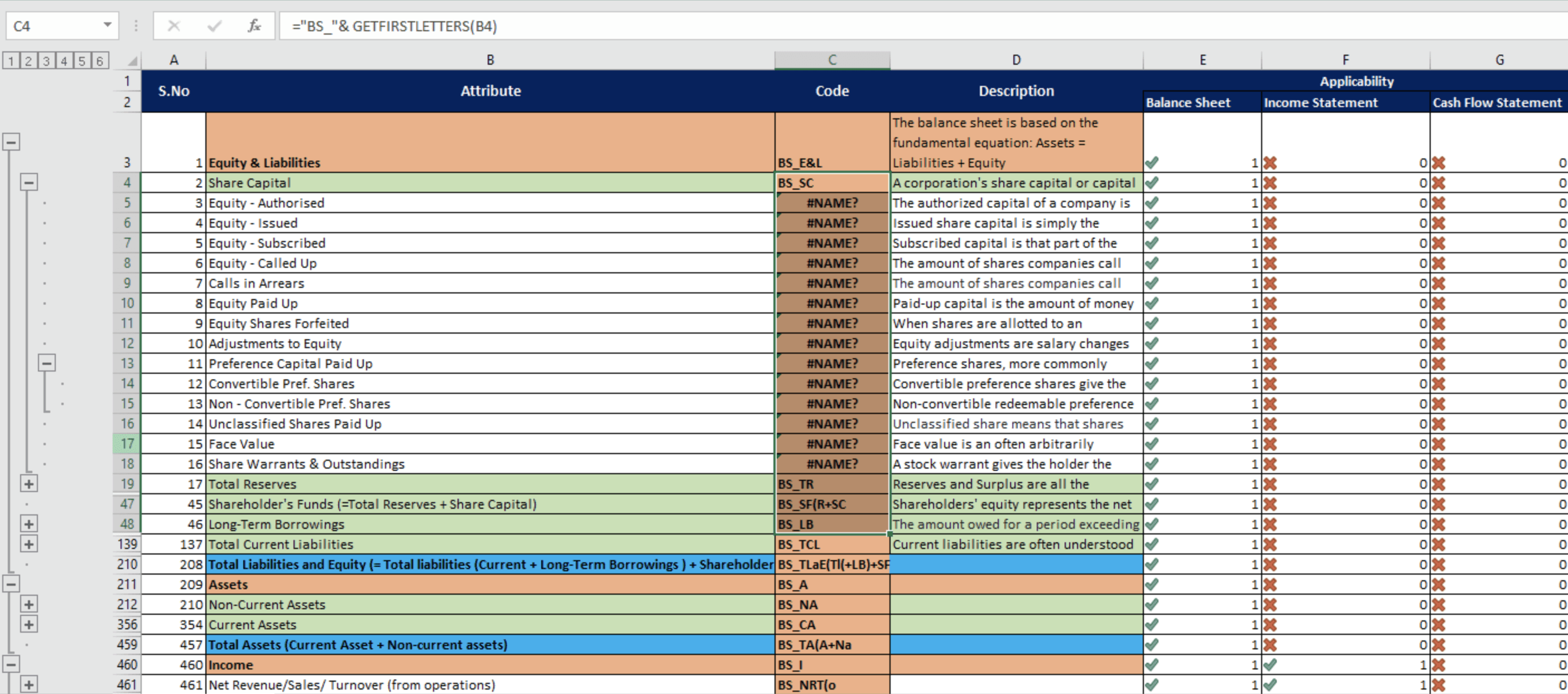

Financial statements (Income Statement, Balance Sheet, & Cash Flow Statement) are key to investigating the financial health of any commercial organization.

Problem

With continually emerging industries and customer segments, banks must constantly update their financial statement templates. Additionally, these templates must adhere to numerous global, local, and organizational regulatory compliance policies.

Currently, all activities related to managing financial templates—authoring, documenting, configuring, and sharing—are performed manually using standard office suite tools.

Although familiar, these tools hinder transparency in the origination process, increasing the likelihood of errors and operational inefficiencies. Ultimately, this lengthens the loan closing time and impacts the profitability of banks.

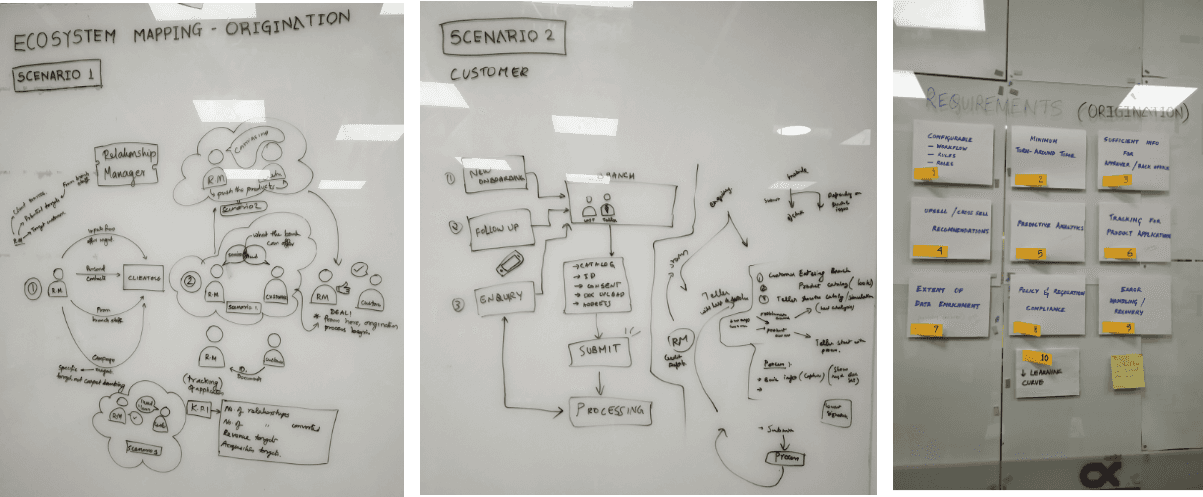

User Research

A remote workshop was conducted with Finacle stakeholders, product owners, ICICI Bank admins, and relationship managers. My research encompassed:

Understanding the current process of creating financial templates.

Flow of a financial template across the bank.

Roles and responsibilities of bank employees at different levels.

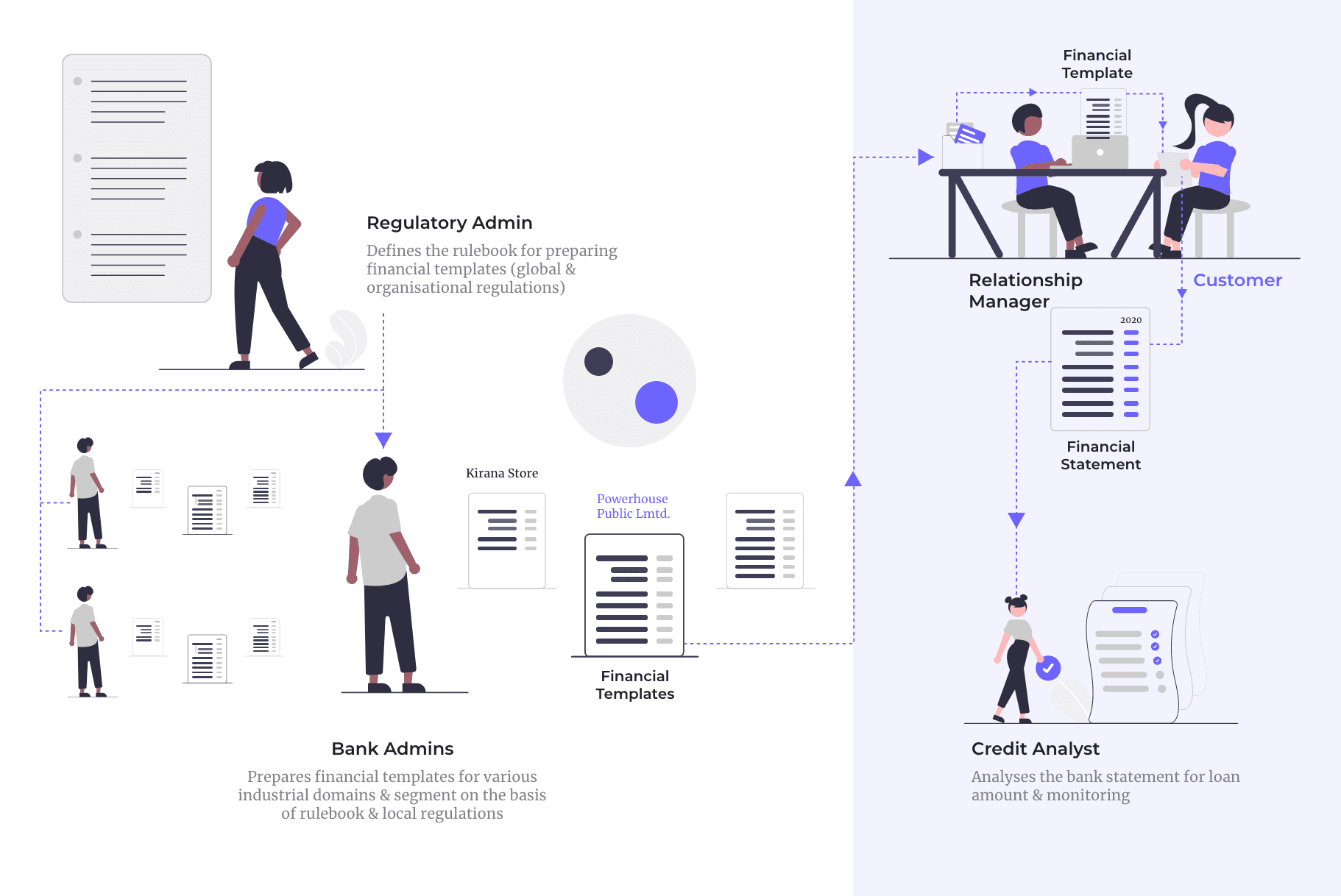

User Profiles

Opportunity Areas

How might we improve transparency in banks' workflow so that financial templates can be managed effortlessly with the least human-errors?

Goals, Tasks & Actions

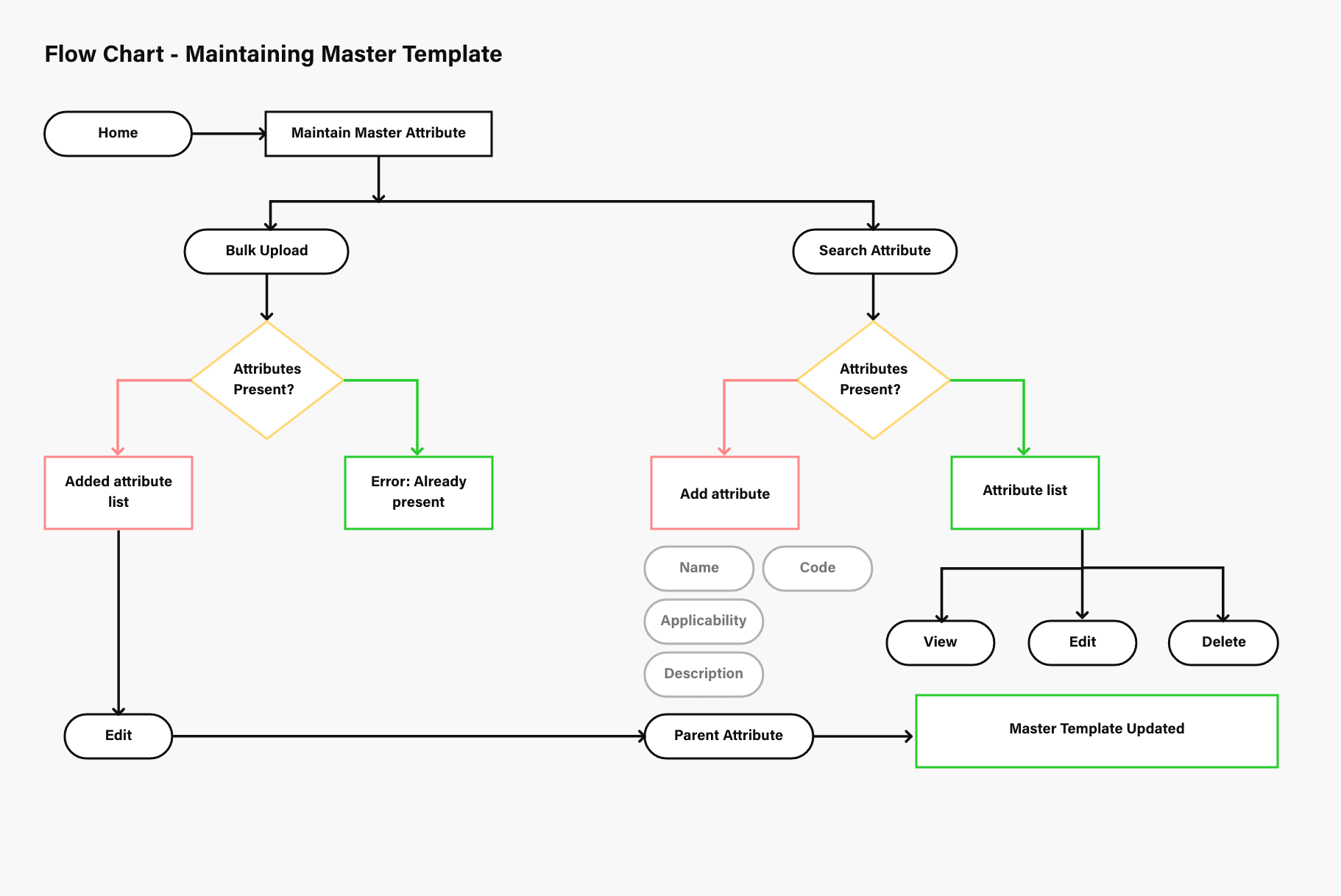

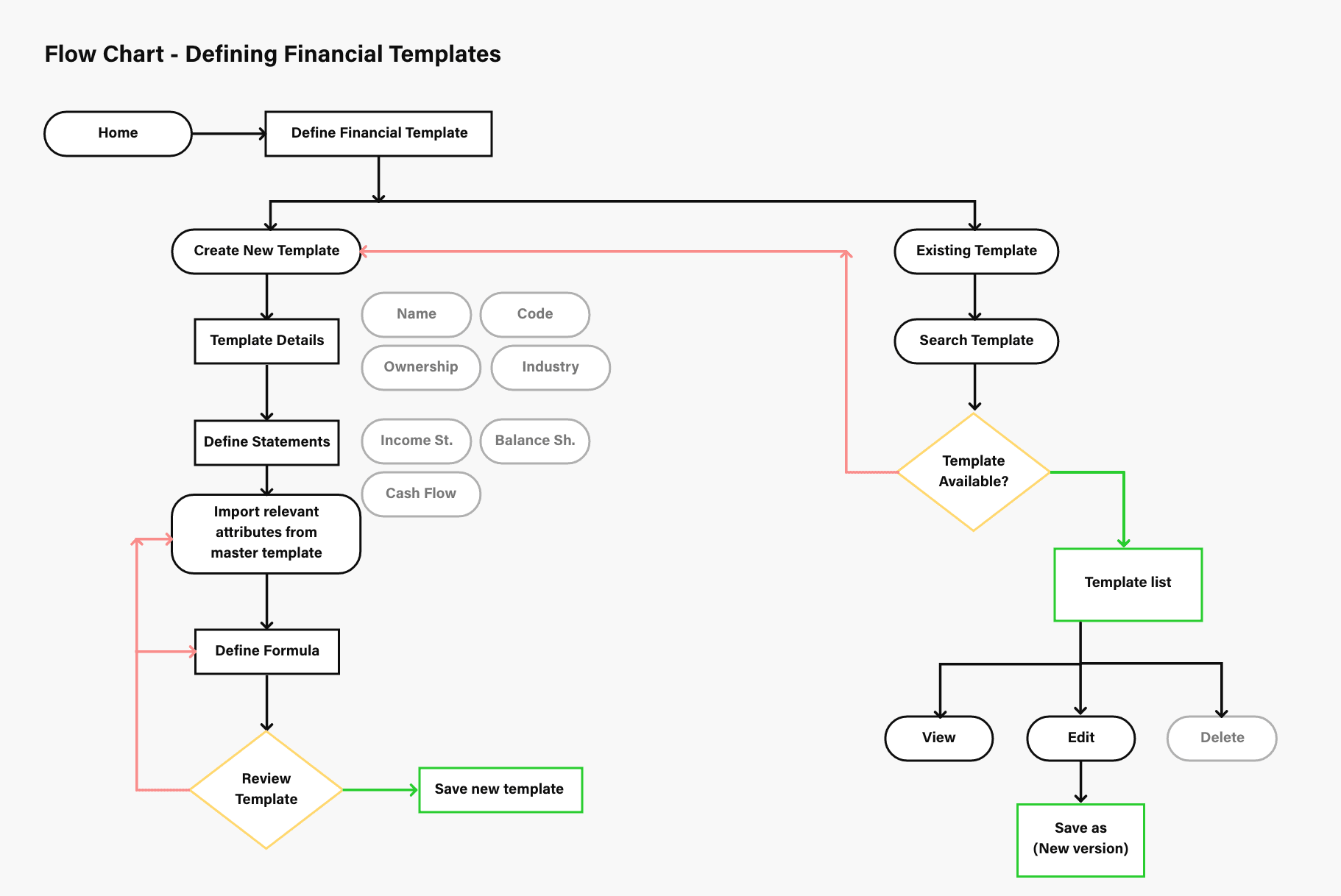

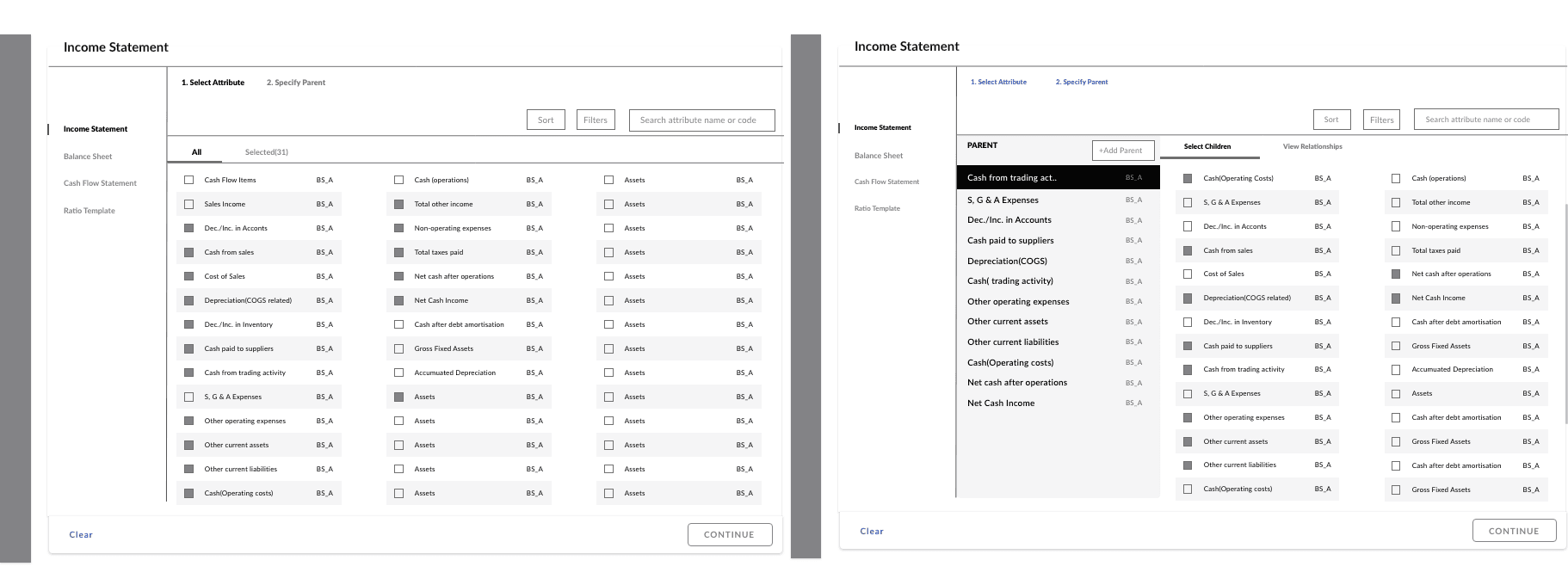

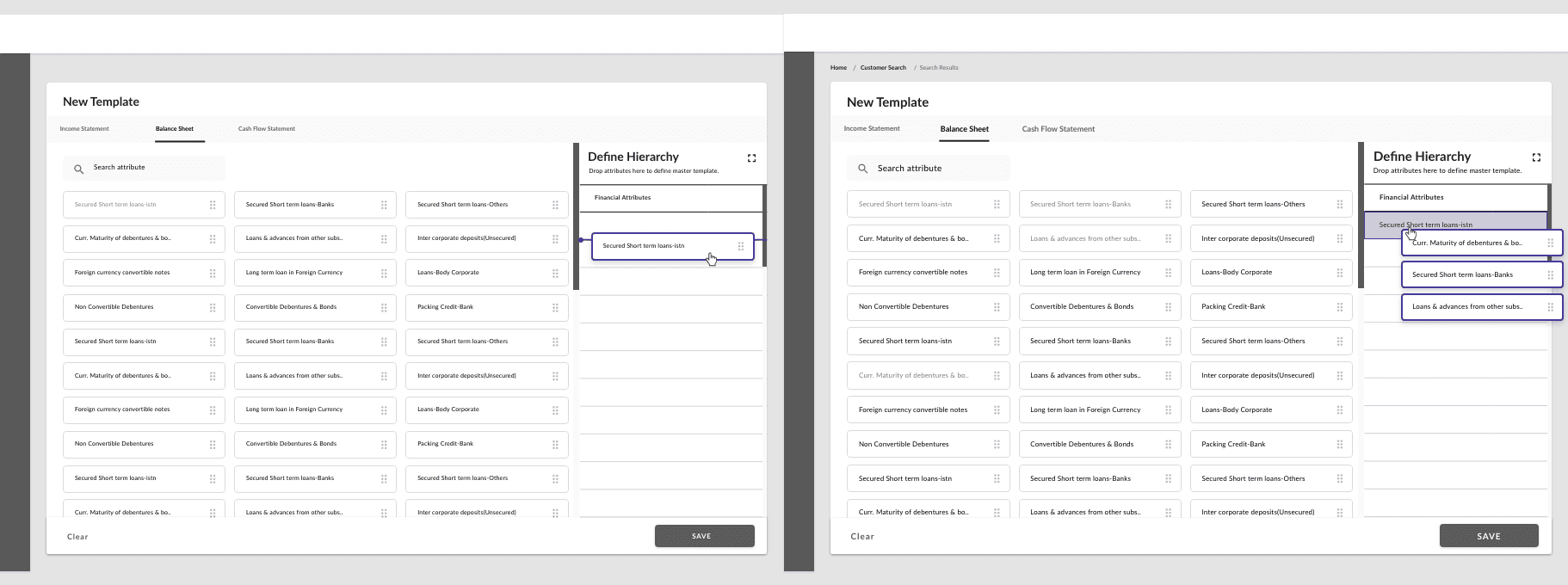

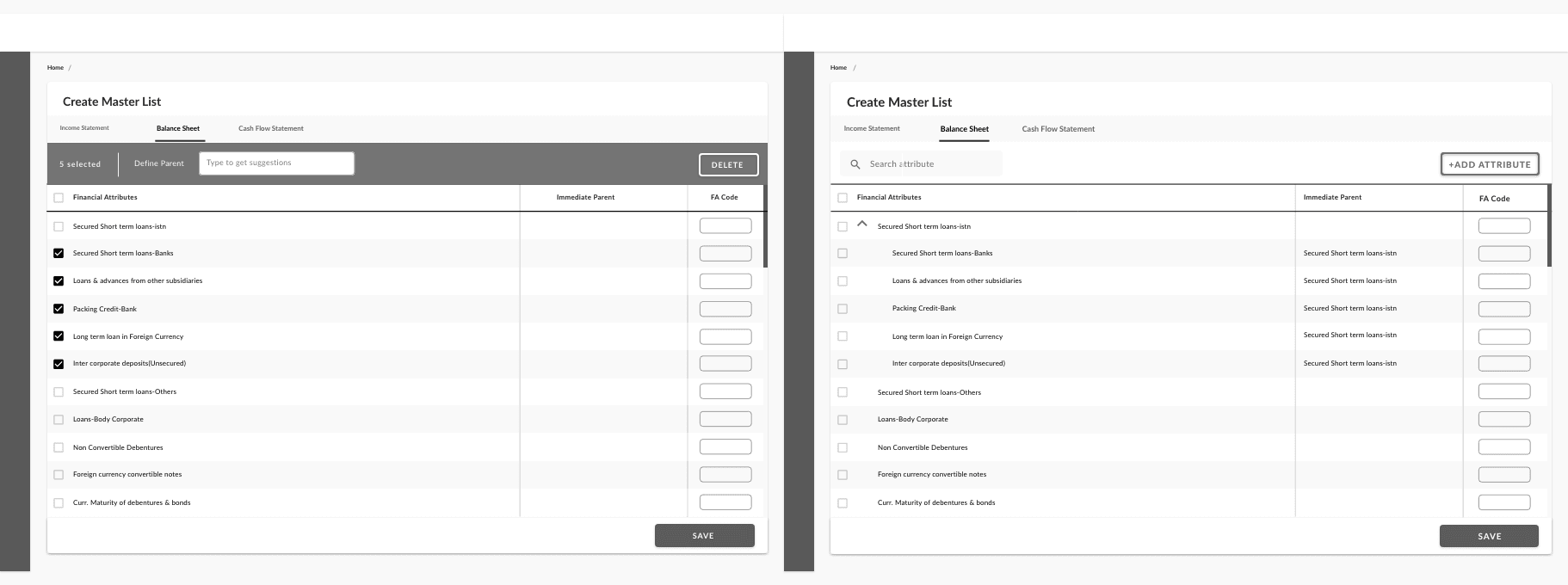

4. Customising an existing financial template.

Select new attributes from master

Deselect existing attributes

Redefine formulas wherever necessary

Conceptualization

Solution