FRAMER

Overview

CARS24 is second-hand used car marketplace. And to be able to afford a car ~70% of users required loans. I worked with the consumer finance team at CARS24 for almost 2 years to make the loans more accessible for a used-car buyer. However, there were several macro & micro problems associated to do doing so.

Why was speed important?

Loan-related issues ranked as the second highest reason for customers canceling their car bookings after test-drives.An in-depth analysis of loan issues helped pinpoint actual user problems:

Uncertainty surrounding loan approvals

Inconsistencies in offer communication.

On average, the time taken to deliver a car (after a test-drive) with finance involved was ~ 5 days, compared to less than 1 day for non-finance customers.

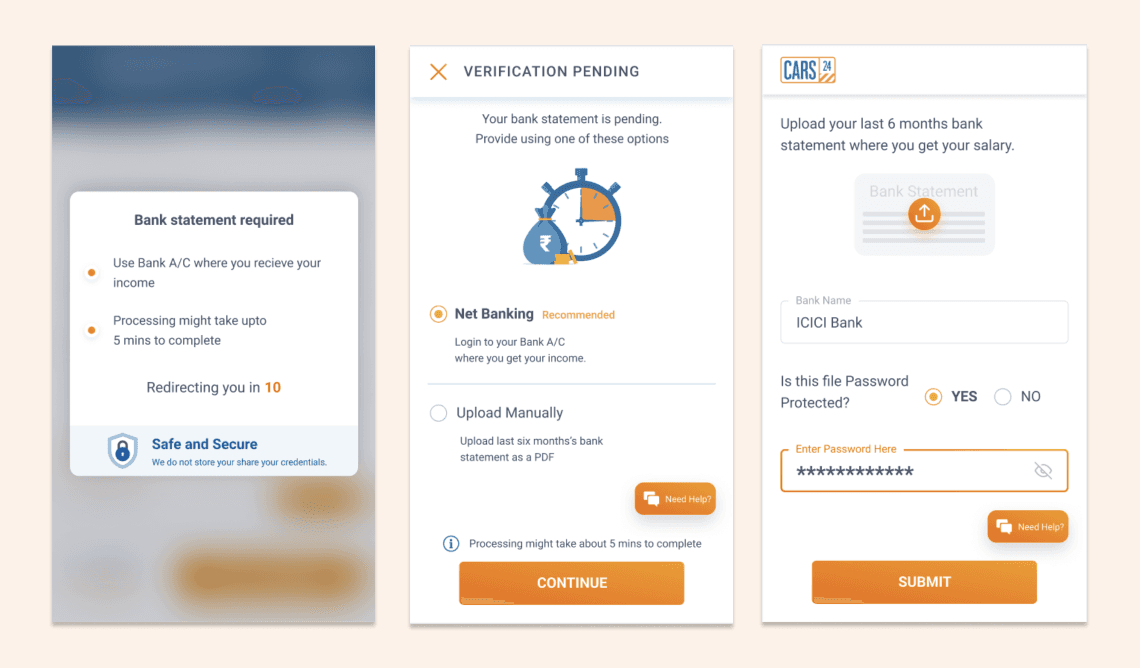

The bottleneck: Bank statement

Upon investigation into prolonged loan approval times, the primary hurdle was acquiring bank statements from users. Banking data was crucial for categorizing customers by risk profile, enabling the prioritization of on-ground and credit team efforts. Our data science team had implemented a decision engine capable of classifying users into green, amber, and red risk profiles.

Users in the green category could be approved solely based on their bank statements, streamlining their experience akin to cash-paying users. However, the engine couldn't identify these users until their bank statements were provided.

Car bookings were being affected due to the existing flow of sharing bank statement

Despite our product's feature allowing users to share bank statements before booking, most statements were still shared manually, leading to a cumbersome back-and-forth process between agents and customers. This impacted car bookings as well.

Insights from user research

What motivates users to share the statement?

Delving deeper into this research question helped us uncover a task framework that users followed to share their bank statements:

Realization of the need for banking

Evaluation of options to share bank statements

Delving into details

Fulfilling the requirements

Expectation of feedback for the transaction

We utilized this framework to formulate various hypotheses at different stages of the user journey. Subsequently, we tested the designs based on these hypotheses using A/B testing

Realisation of the need for banking

Observations:

Tries to understand why bank statements are required

Second-guesses if sharing bank statements with CARS24 will be secure

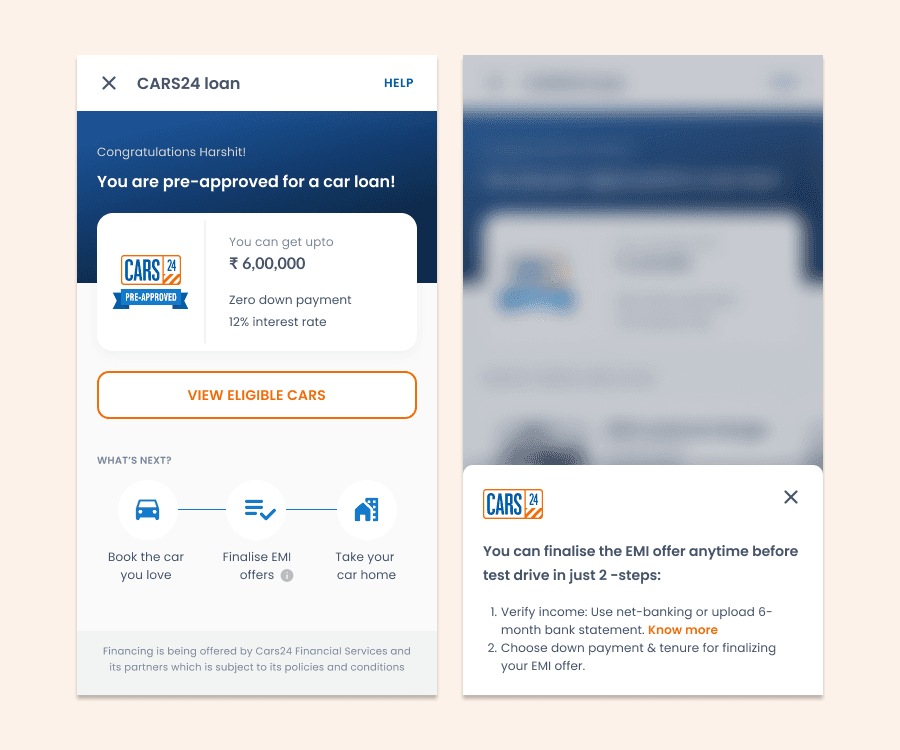

Hypothesis: Educating users about the loan process right from the start would better prepare them for sharing bank statements at a later stage.

Impact: ToF pre-approved users shared approximately 32% more banking information on the app compared to users pre-approved from checkout.

(User cohort: asked for banking only after booking completion;)"

Hypothesis: Letting users move ahead with their car booking while just priming them about banking would prepare them to share at a later stage while not distracting them from their primary goal.

Impact:

90% users skipped banking without submitting.

However, the conversions of banking after booking (for users pre-approved from checkout) were 2x higher than the users asked to do banking mandatorily before booking.

Obviously, booking conversions were higher for this cohort of user.

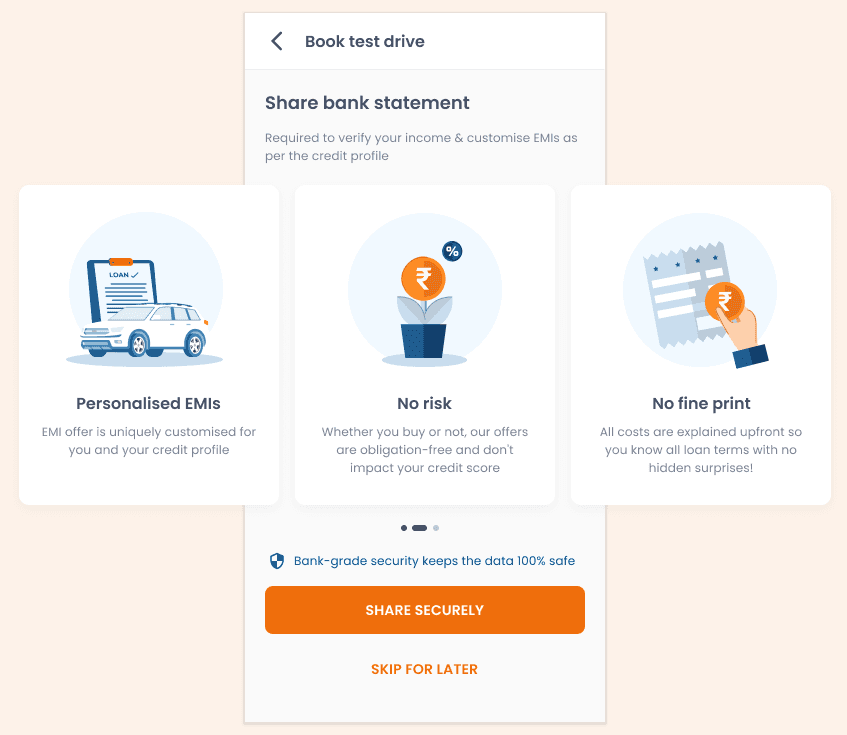

Hypothesis:

Users would be more committed to share banking once they have booked the car.

Explaining how sharing banking impacts their car purchase experience would motivate users to share.

Evaluation of options to share bank statements

Observations:

Looks at different ways of sharing bank statements

Tries to evaluate each method on the basis of convenience & familiarity

Delving into details

Observations:

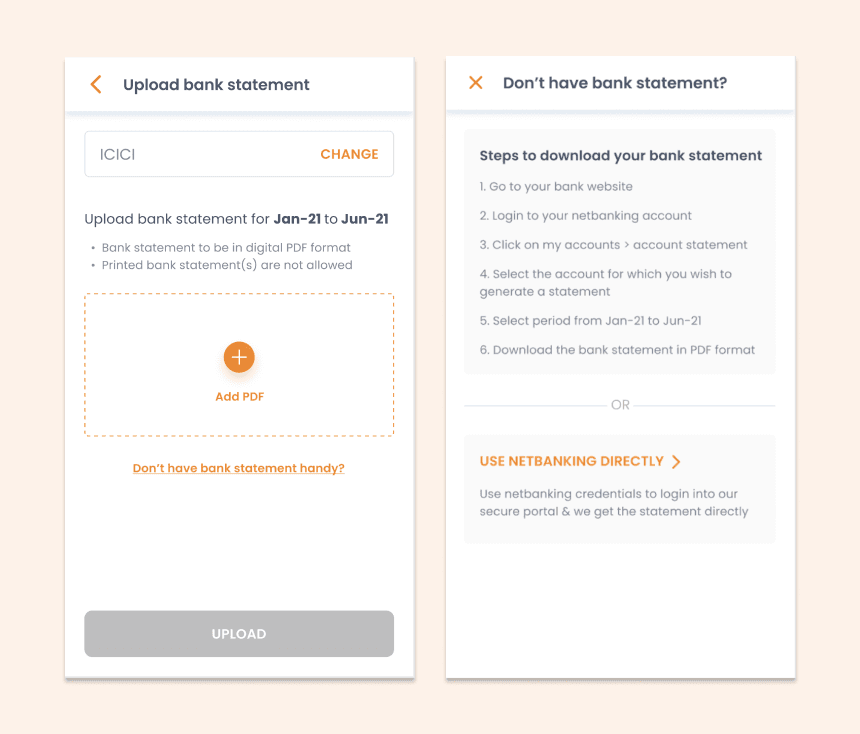

It was evident from data that users preferred the PDF upload method for sharing. Therefore, we prioritized enhancing the user experience for uploads. Research indicated that users often shared incomplete bank statements. We began with the following phased approach:

Communicating specific months instead of a range to users.

Assisting users in downloading bank statements from their net-banking accounts.

Introducing nudges to encourage users to directly use their net-banking credentials to share bank statements

Fulfilling the requirements & receiving a feedback

Impact over 3 months

02

~26% increase in banking done on app directly

Further way ahead?

Still, most users interested in finance were dropping off while trying to share bank statements with either of the two options but were not able to.

Uploading bank statements was still effortful since the user had to get the correct bank statement manually, and sharing net-banking credentials had its own security apprehensions in the minds of users. This led the entire product team to ask if there was an easier, secure way to get banking done.

The answer was Account Aggregator. And I was really fortunate enough to work on something that could shape the future of data sharing

After several rounds of discussions with PMs, developers & the compliance team; we finally concluded with this particular flow.